How to proactively manage a lending portfolio in uncertain times

We analysed a random sample of 1,820 SMEs across multiple industries using our unique approach to resilience analysis. Seven distinct archetypes emerged. These archetypes outline clear trends and traits which provide valuable insight to help leaders proactively segment and manage SME portfolios in uncertain economic conditions.

The pandemic emerged at an extraordinary speed, catching everyone by surprise. Whereas the 2008 financial crisis - the last period of major economic shock - unfolded in several stages between 2007 and 2009, within weeks of China announcing the first Covid cases governments all over the world introduced lockdowns to slow the spread. Economic activity ground to a halt, output dropped at a record pace and businesses scrambled to adapt. Many thought lockdowns would last a couple of weeks, not a couple of years. Digital transformation accelerated by three to four years in the space of a few months and emergency government support damped the immediate economic impact, especially for SMEs.

UK businesses were already on their toes when the pandemic hit having spent a few years anticipating the challenges and opportunities from Brexit. Two years later, lockdown eased just before the war in Ukraine began in the midst of rising inflation and energy prices.

Despite the consistent uncertainty, the data supports an overarching narrative of resilience vs fragility, with varying degrees in between, rather than one of broad economic catastrophe. Some SMEs have adapted and thrived in the face of challenges, some have remained relatively stable and others have barely hung on. As the effects of government support during the pandemic wear off, the foresight to distinguish between resilient and fragile businesses today (and for whatever tomorrow may hold) is critical for lenders and corporates alike.

Post-Pandemic Fog

Anticipating the impact of lockdown on the business community and broader economy, governments responded to the pandemic by introducing a range of support measures the likes of which had never been seen. In the UK, Chancellor Rishi Sunak spent £70 billion on a furlough scheme to protect jobs, while the Coronavirus Business Interruption Loan Scheme (CBILS) and the Bounce Back Loan Scheme (BBLS) - the latter targeted small and medium-sized enterprises (SMEs) - distributed over £80 billion of government-backed loans to help companies survive. The total cost of the stimulus provided by the Treasury surpassed 30% of the gross domestic product in 2020, according to the International Monetary Fund.

While it averted the nightmare scenario of a health crisis giving birth to an economic crisis, government support artificially suppressed default rates among SMEs. The easy access to funding helped ‘zombies’ - a term commonly used to describe companies that are stagnant and propped up by favourable lending terms - to survive. Businesses that were not zombies used government support in different ways. This provided much-needed breathing space for some businesses to adapt their business models while, for others, it simply increased a debt burden they may be unable to pay. As governments have withdrawn support, default rates have begun to rise, and it is unclear how far they will go before reverting to the mean.

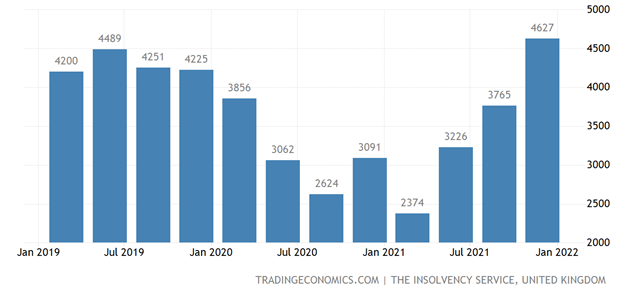

Bankruptcies in the United Kingdom increased to 4627 Companies in the fourth quarter of 2021 from 3765 Companies in the third quarter of 2021.

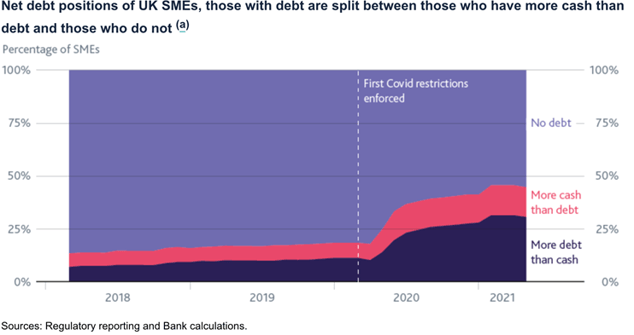

Research by the BoE into the impact of Covid on SME finances shows that nearly a third have a high debt-to-cash ratio, compared to just over 10% before the pandemic. At the same time, approximately 15% of SMEs managed to improve their cash-to-debt ratio during the pandemic, almost twice as many as before the first Covid restrictions came into force.

Resilience: An Approach to Portfolio Analysis

To thrive in this environment, lenders must have deep and early insight into the impact of these trends on their SME lending portfolios as well as how each SME is poised to respond. The ability to quickly identify the correct signals of underlying strength or weakness in their portfolios is critical for lenders who need to take early and effective action. In the past, stock market prices, credit scores or sector trends have been used as benchmarks to measure company or industry segments performance. However, there is no single predictor or metric that is sufficiently tailored to today's context, providing relevant insight into an SMEs ability to adapt and respond

We have developed an approach to portfolio analysis we believe provides much needed insight today: our approach to resilience analysis starts with the SME Z-score and combines it with core financial metrics. Using this approach, we identified archetype-based trends and traits based on an SMEs starting position the year before the pandemic began and their performance, or behaviour, in the first year of the pandemic. While some companies started the pandemic with stronger business fundamentals than others, no business had sufficient time to prepare for the existential threat posed by the pandemic nor could they have anticipated the extraordinary levels of financial support offered by governments across the world. Every business had a unique starting point when the pandemic hit and took a different approach to managing their way through extreme uncertainty.

We applied our approach to resilience analysis to a sample of 1,820 SMEs spread across seven industries in the UK.

Across these diverse businesses, seven archetypes distinguished themselves through common traits, these include: Resilients, Emerging, and Survivors (these three categories represented approximately two-thirds of the sample), Ghosts (represent approximately one-sixth of the sample) and Fallen Angels, Fragile, and Zombies (combined represent approximately one-sixth of SMEs studied). Like characters in a story, these seven profiles each started from a unique baseline with particular strengths and weaknesses, followed a unique journey and displayed certain patterns and behaviours which shaped how they adapted - or not - to the existential shock of the covid pandemic.

SME Archetypes: Traits and Trends

Resilients: Resilient companies started off in a relatively strong position back in 2019 (medium risk or better) and, through sound management and solid financial performance, improved their risk scores between 2019 and 2020. On average, they were able to increase their turnover by approximately 18% and expand EBITDA margins by an impressive 46%. As a result, they were able to double net income year on year. They accomplished this with relatively modest increases in debt while reducing their overall debt to asset ratio by 22%. Overall, they entered the first year of the pandemic in a strong position and ended that challenging period in an even stronger position.

Emerging: Like many memorable characters on epic journeys, emerging companies did not originally stand out. Their risk profile and financial performance in 2019 placed them in the medium to high-risk category. However, on average, in the first year of the pandemic they managed to increase their EBITDA margin by 50% and retained earnings by an extraordinary 78% using government support to mitigate near term pressures (long term debt rose by 167% from a low base while short term debt fell 29% from a high base) and create the flexibility to adapt and thrive during the pandemic. As a result, they had the highest average improvement in SME Z-score of any archetype.

Survivors: Before the pandemic, Survivors enjoyed a strong financial and risk position. This helped them absorb the financial shocks of the pandemic. Between 2019 and 2020, Survivors matched a slight drop in turnover with a comparable reduction in operating costs and a modest increase in debt was matched by a similar increase in assets. Their EBITDA margin fell by 14% but the impact was limited as Survivors had the highest EBITDA margin of any archetype before the pandemic began. Net income also dropped year on year, as did their SME Z-score. Survivors represented approximately half of the SMEs we studied.

Ghosts: Despite starting the pandemic in a high risk category and with the second worst SME Z-score of any archetype, Ghosts suffered only modest financial declines in the first year of the pandemic. A 1% decline in turnover was matched by a 1% decline in operating costs. An 11% increase in total debt was matched by a 12% increase in assets. However, Ghosts have over 80% of their debt in short term maturities and 80%+ debt to asset ratios. When combined with low (3% on average) net income margins, Ghosts are already operating closed to distressed levels and have little room to manoeuvre a path back to healthy territory. They make up the second largest group of SMEs in our sample.

Fallen Angels: Despite a strong financial and risk position in 2019, Fallen Angels experienced the largest drop in SME Z-score amongst all archetypes as they suffered from an inability to adapt their business models to the crisis. On average, Fallen Angels experienced a 25% drop in turnover, 113% collapse in EBITDA margin, and a 28% increase in total debt as a percentage of total assets. Fallen angels almost doubled their short-term debt and more than halved their long-term debt, putting themselves under extreme pressure in the short term which translated into their 2020 net income dropping into the red.

Fragile: The pandemic has been harsh for Fragile companies. They experienced a 50% drop in Turnover, an extraordinary 290% collapse EBITDA margin, and a catastrophic 1000% drop in net income. With high levels of existing debt, of which 95% was in short term obligations, the additional 15% growth in short term maturities applied further momentum to their downward trajectory. On average, their high debt, coupled with a 35% decline in assets took the average Fragile debt to asset ratio up to 115%, the highest of any archetype. Fragile companies already had an average SME Z-score in the high-risk band before the pandemic. They suffered the second largest drop of any archetype, just behind the Fallen Angels, to end up in the Distressed risk band where the vast majority of these SMEs are at high risk of collapse.

Zombies: While the damage to their financials was not as severe as what Fragile and Fallen Angel SMEs suffered, Zombies were already operating from the lowest risk category of any archetype. A 40% decline in EBITDA margin simply took that metric further into the red. In 2020, Zombies quadrupled the losses they suffered in 2019. With 93% of their debt in short term maturities and an average debt to asset ratio of 92%, we expect Zombies will finally succumb in line with the rollback of government support.

A Dynamic, Scalable Solution

We believe these insights are relevant and timely for lenders seeking to understand how their portfolios might perform as SMEs adapt to life after government support and the pendulum of defaults inevitably swings back before stabilising. Each archetype will continue to develop and evolve but they will do so within the constraints of their character and journey to date.

Executing this analysis frequently enough to track evolving trends can be time consuming, costly and complex, especially at scale. From gathering and standardising data across a portfolio of hundreds or thousands of SMEs, to identifying relevant benchmarks, deriving actionable insight and refreshing the exercise periodically; the steps required to go from idea to results can seem daunting and prohibitive.

We built the Wiserfunding platform with these types of challenges in mind. Grounded in over five decades of academic research, benefitting from cloud based, API enabled architecture, and supported by a team of experts, our clients have access to our easy to use, cutting edge platform solutions that enable them to execute the credit risk analysis and portfolio insights that can be the difference between identifying the best SMEs and delivering top quintile performance or suffering from a portfolio fraught with weak and fragile businesses hiding amidst uncertainty and confusion in a post-pandemic economy.

Our solution builds on the rich academic history of our co-founders, Professor Edward Altman and Dr. Gabriele Sabato. In developing our resilience analysis, we have expanded on the McKinsey article, The emerging resilients: Achieving ‘escape velocity’.

To find out how Wiserfunding can help manage risk in your lending portfolio, get in touch today.