Blog

Navigating the New Landscape

The implications of removing the SME supporting factor for financial institutions

With 25 UK energy providers now in administration, the impact on consumers is significant. This article highlights the importance the sector’s resilience

This week, we released research into the UK energy sector, which highlighted systemic shortcomings in the assessment of dozens of UK energy providers. Our data revealed that the majority of defaulted UK energy providers in 2021 were in financial distress years before price rises came into effect. Energy shocks simply exposed the vulnerabilities that were hiding in plain sight for many years.

With the war in Ukraine triggering another significant shock to the industry, the findings raise fresh concerns about the underlying health of the sector. They also highlight competent risk management, effective due diligence and sound regulation as the critical factors in future-proofing UK energy providers.

While the UK government reconsiders how to meet demand for energy in the long-term, following a move to phase out Russian hydrocarbons, we are calling for domestic suppliers to ensure their business fundamentals are sound to avoid future financial distress and more defaults.

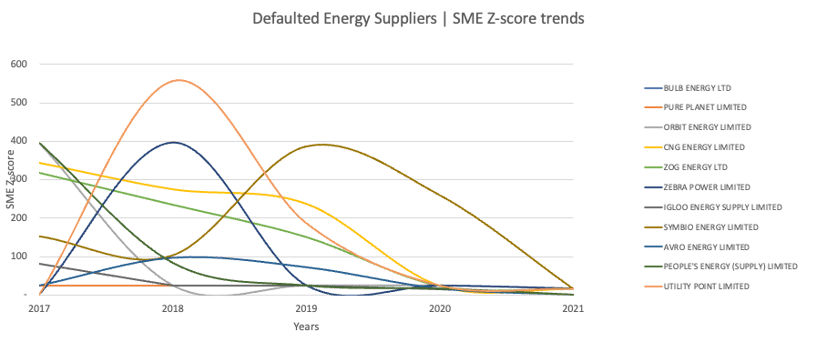

Breaking down the data

Our innovative technology and credit risk models generate an SME Z-Score, along with financial and risk metrics, based on a company’s multi-year performance. The SME Z-score ranges from 0 to 1000 with scores below 100 indicating a company is in significant financial distress and close to defaulting. A score between 101 and 250 confirms a company is high risk as its credit risk profile is weak and the likelihood of becoming distressed within the next 12 months is high. A company does not become low risk until it exceeds a 450 SME Z-score.

Using a mix of financial and unstructured data, as well as macroeconomic variables, we identified distressed energy providers that could have been identified and strengthened years in advance of going bust.

While there is no doubt that the impact of rising gas prices, which climbed by 250% in 2021, contributed to many energy providers’ exiting the market, our findings show that this was not the primary cause of their downfall.

Of the 11 insolvent energy companies that we analysed, over half, including Bulb and Total Energy, were classed as being at high risk of default within just 18 months of their initial incorporation. Most companies showed serious vulnerabilities in 2019, one year before the official energy crisis began and only months after raising substantial funding from institutional investors.

The war in Ukraine will further stress energy prices. Our study demonstrates that business fundamentals can be proactively identified and managed ahead of and independently to macro and geopolitical shocks. Getting the basics right when it comes to risk management and sound business fundamentals will significantly improve the energy sector’s ability to navigate macro stresses.

|

Wiserfunding energy company data

|

||||

| Company | Default Date | SME Z-Score 2019 | SME Z-Score 2020 | SME Z-Score 2021 |

| Avro Energy | Sep-21 | 97 | 72 | 16 |

| Bulb Energy | Nov-21 | 24 | 24 | 16 |

| Igloo Energy | Oct-21 | 24 | 24 | 16 |

| Neon Reef | Nov-21 | 396 | 24 | 16 |

| Orbit Energy | Dec-21 | 24 | 24 | 16 |

| Peoples Energy | Oct-21 | 83 | 24 | 16 |

| Symbio Energy | Oct-21 | 386 | 259 | 16 |

| CNG Energy | Dec-21 | 238 | 24 | 16 |

| Utility Point | Sep-21 | 186 | 24 | 16 |

| Zebra Power | Nov-21 | 24 | 24 | 16 |

| Zog Energy | Dec-21 | 151 | 24 | 16 |

Building on weak foundations

Green energy pioneer Bulb rose from start-up to the UK's seventh biggest energy supplier in just six years. However, this growth did not translate into robust financials. Since 2015, Bulb maintained an alarming SME Z-score below 100, demonstrating extreme fragility - five years before its collapse in 2021. While the company recently blamed rising costs for its demise, this lack of resilience was evident in the data over half a decade ago.

Other energy providers we analysed suffered similarly avoidable fates. Orbit, Igloo and Avro have not had an SME Z-score of above 100 since 2017. In particular, Avro Energy, with a customer base of over 1.2m at one stage, has not had an SME Z-score above 100 since its inception in 2015 and operated at the edge of default for half a decade. They eventually collapsed in late 2021 owing $90M to customers.

Our research shows that providers with much stronger risk profiles, such as E.ON, EDF and British Gas, have so far managed to mitigate the short-term distress of price fluctuations through more resilient balance sheets and business strategies.

However, Ofgem’s plans to introduce reforms and tighten regulation came too late for many. Had it been introduced sooner, tougher regulation could have ensured providers had the necessary financial resilience to weather fluctuation in energy markets. It’sparticularly concerning that new providers were able to enter the market when their business models and financial health were clearly not robust enough to navigate industry challenges.

Were investors sold a dream?

While many challenger brands entered the market with the promise of cheaper bills and green energy for consumers, we must ask how these providers convinced lenders and investors to continue deploying vast sums of capital when their resilience was highly questionable. For example, in late December 2019 Igloo Energy received £20m from Osaka Gas Co. to help accelerate growth, despite having an SME Z-score of just 24. In fact, it failed to score over 100 since its incorporation in 2015 and operated from a position of financial distress every year.

The question remains as to whether investors were unable to correctly assess the existing financial risk of these companies; or whether they were allowed to make highly speculative investments in public utilities at the expense of the public interest.

Identifying risk at a company level will improve the resilience of business models and financial performance, ensuring providers can weather future macroeconomic and geopolitical storms. Consumers cannot continue to pay the price for failings in the ability of regulators and investors to correctly assess and manage risk.

*Data recording Wiserfunding’s SME Z-Score (0-1000) of selected defaulted energy companies

Applying learnings to today

The horrific invasion of Ukraine is a new and significant challenge for the energy industry, which was already struggling with supply issues and wholesale price increases.

But while macroeconomics are a substantial trigger, the truth is that many energy companies have been financially fragile for a while and propped up by large, speculative investments. This latest geopolitical shock will have a further knock-on effect as a macro risk but won’t lead to the default of UK energy providers on its own. Providers can weather these storms, providing they have effectively assessed and mitigated risk at a company level, building resilient business strategies and balance sheets.

With 25 UK energy providers now in administration and more challenges still to come, the expected impact on consumers is significant, highlighting the critical importance of monitoring and improving thesector’s resilience for the long term.

You can find more information on the SME Z-score and our Credit Risk Models here.

The implications of removing the SME supporting factor for financial institutions

As public markets wrestle with macroeconomic risks and difficult national and regional events, the bull run of the past decade shows signs of coming...

Wiserfunding's most recent blog post discusses the benefits of increasing support for SME funding through capital markets.